Download the FREE Business Credit Blueprint for Business Owners

The No B.S. Business Credit Blueprint

You're profitable. Your personal credit is solid. So, why do banks keep saying no?

Banks care about something called your "fundable profile." If you don’t know what that is (or if you don’t know how to build yours), you're going to get denied.

Enter your info below

Trusted by

Most business owners never learned how banks actually evaluate applications.

Your business training taught you to serve customers and make money. Nobody taught you about fundable profiles or the three-layer system banks use.

Most get rejected because of fixable compliance issues

The majority have zero business credit (relying only on personal)

Very few understand how banks actually score applications

This guide shows you exactly how to build a fundable profile that gets you approved for real credit, without putting your personal assets on the line.

The Three-Layer System Banks Actually Use

Most business owners spend all their time on financials (revenue, profit, cash flow) and no time on these three layers that actually determine approval.

Identity

Your business's "paperwork identity" across all databases banks check. Secretary of State registration, IRS records, USPS address verification, 411 directory listing, and D-U-N-S number registration. If this layer has gaps or inconsistencies = automatic red flags.

Credit Profile

Your business credit across the three major bureaus: Dun & Bradstreet Paydex score, Experian Business Intelliscore, and Equifax Business Payment Index (all rated 0-100). Without this layer = you're applying as a startup every time.

Banking Behavior

How you manage your business bank account: average daily balance ratings, transaction patterns, overdraft history, and length of banking relationship. This layer separates good credit from great credit.

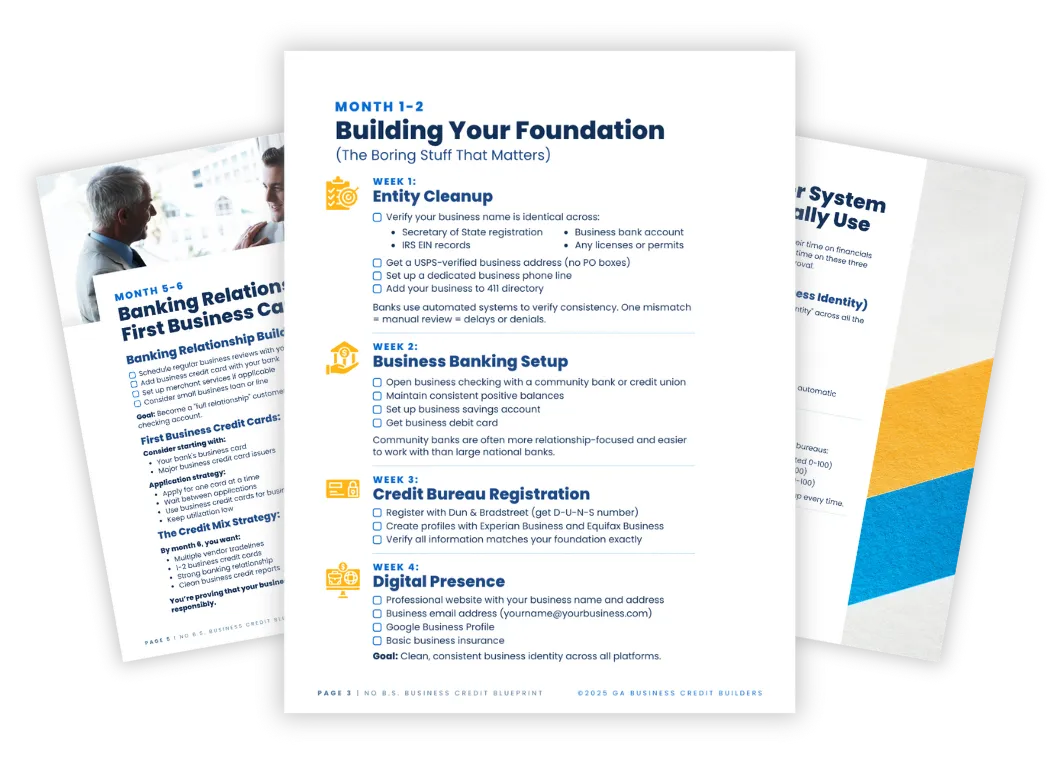

Your Month-by-Month Blueprint

Months 1-2

Building Your Foundation

The boring stuff that matters. Entity cleanup, business banking setup with community banks, credit bureau registration, and digital presence. Goal: Clean, consistent business identity across all platforms.

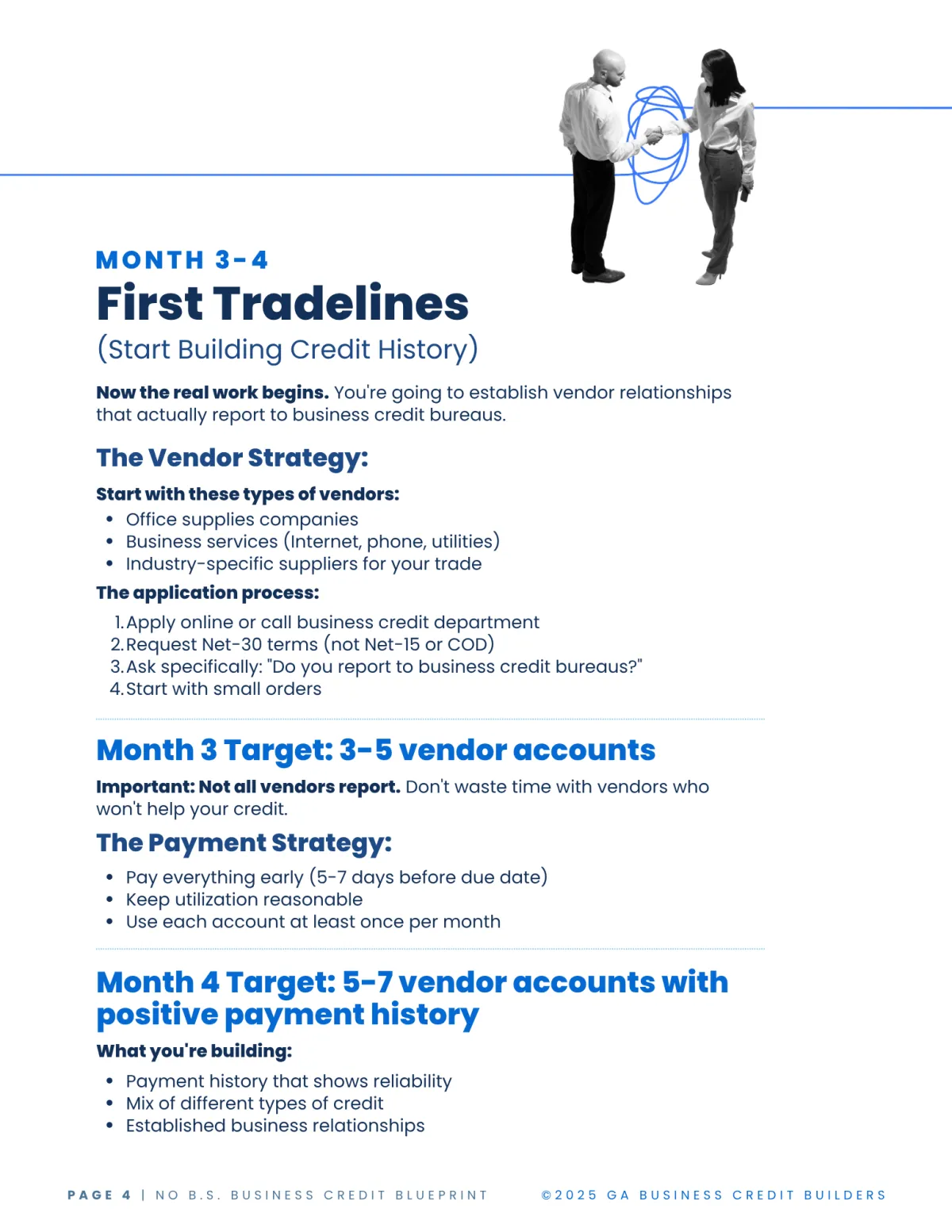

Months 2-4

First Tradelines

Establish vendor relationships that actually report to business credit bureaus. Target: 3-5 vendor accounts with Net-30 terms, growing to 5-7 accounts with positive payment history.

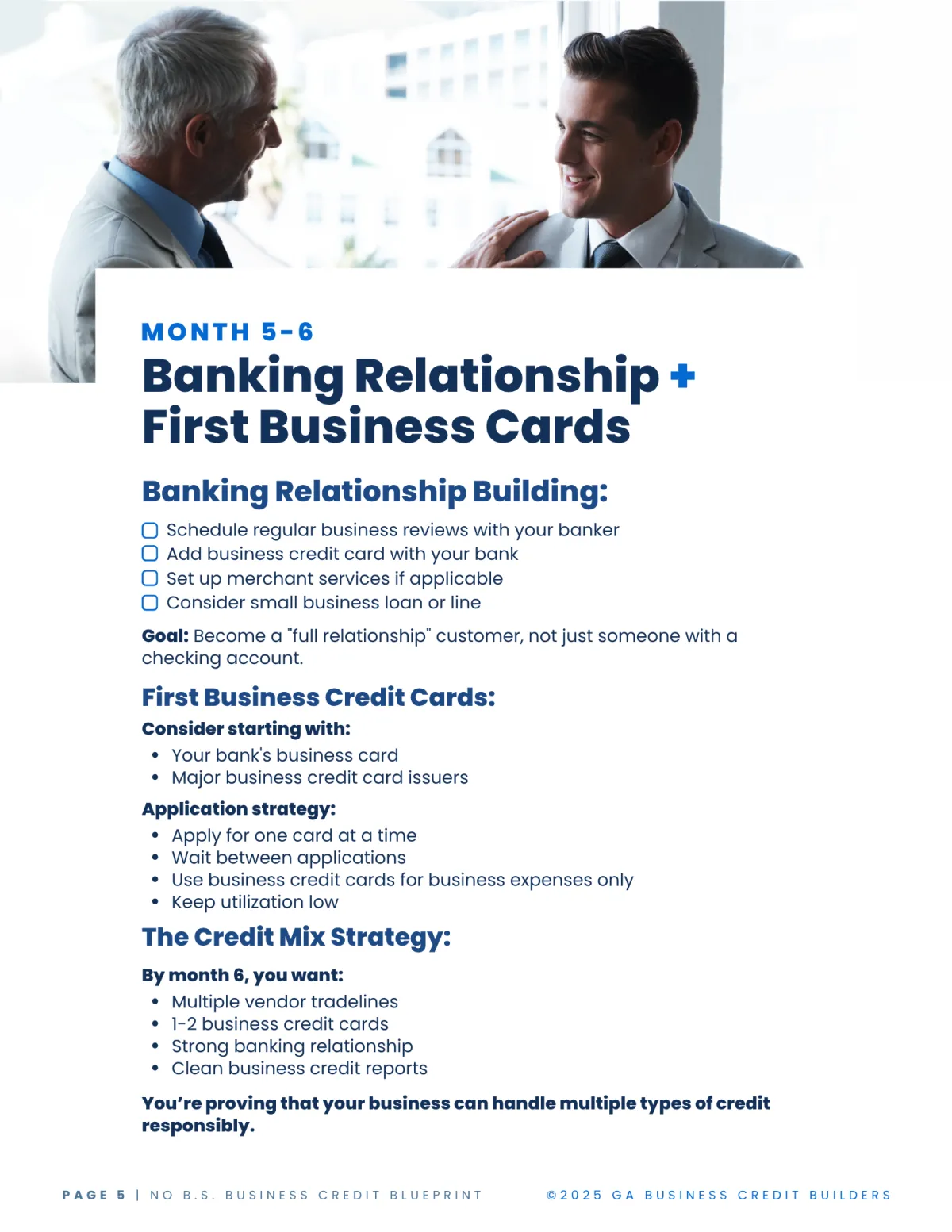

Months 5-6

Banking Relationship + First Business Cards

Become a "full relationship" customer, not just someone with a checking account. Add business credit cards and strengthen your banking relationship.

Months 7-12

Credit Stacking + Optimization

Access real credit. Apply for higher-limit cards, term loans, and lines of credit. This is when you can start applying for serious funding without personal guarantees.

Kind Words From Our Clients

"Cody and his team have been a huge help to me in my business. I'm looking forward to a long and prosperous relationship with GA Business Credit Builders!"

- Francesca C.

"The team at GA is personable, reliable and absolutely outstanding at what they do. I would give more than 5 stars if I could! You all have been amazing with assisting us with our business model and ideas of what to look at when scaling for growth opportunities!"

- Leta S.

"They truly listen and take the time to understand your goals, offering tailored advice and strategies that are both practical and impactful. The wealth of knowledge they bring to the table is remarkable, and I’ve gained so much clarity and confidence in my professional growth within the first few weeks!"

- Jen B.

FAQs

Why do I keep getting denied even though my business is profitable?

Banks don't care about your revenue. They evaluate three layers most business owners ignore: your business identity consistency across databases, your business credit profile (separate from personal), and your banking behavior patterns.

What is business identity consistency and why does it matter?

It's your business's "paperwork identity" - how your name, address, and EIN appear across Secretary of State registration, IRS records, USPS verification, 411 directory, and D-U-N-S number. One mismatch = automatic red flags and manual review delays.

Don't I already have business credit if I have good personal credit?

No. Your business has separate credit reports with Dun & Bradstreet (Paydex score), Experian Business (Intelliscore), and Equifax Business (Payment Index). Without established business credit, you're applying as a startup every time, regardless of how long you've been in business.

How does my business bank account affect credit approval?

Banks analyze your average daily balance, transaction patterns, overdraft history, and relationship length to assess financial stability. Poor banking behavior can kill an application even with good credit scores. This layer separates good credit from great credit.

How long does it take to build a fundable business profile?

The complete system takes 6-12 months, but you can start seeing results in 60-90 days if you follow the right sequence and get your foundation solid first.

Download Your FREE Blueprint Now

Perfect for business owners in construction, auto services, and B2B trades making over $1M who want to understand their fundability and make smart credit decisions.

Copyright 2025 | GA Business Credit Builders | Terms & Conditions